Today’s Silver Reporter Kim Se-gwan | 2023.06.01 05:15

The financial authorities saw the move to reduce drivers’ insurance from July as out-of-sale marketing and issued a warning to the insurance company. In a situation where the overheated driver’s insurance competition has collapsed, it has put the brakes on efforts to reduce consumer benefits.

According to the insurance industry on the 31st, on the afternoon of the 30th, the Financial Supervisory Service asked each insurance company’s product manager and compliance officer to submit their views on whether the driver’s insurance policy was being changed and how to control the outside to the market. sales marketing.

This is because some non-life insurance companies have recently shown a move to add up to 20% of the self-pay for driver insurance traffic accident treatment subsidy and attorney fees insurance from July.

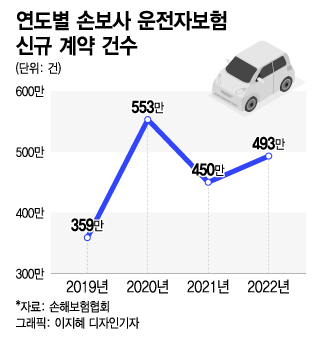

Driver insurance is insurance that covers expenses such as injury or criminal / administrative liability due to a car accident. Unlike car insurance, it is not compulsory insurance. Earlier this year, as the special terms and conditions for attorney appointment fees (hereafter referred to as the special agreement) were released from the exclusive right to use, a number of non-life insurers jumped on the bandwagon. competition to buy driver insurance.

The current special contract for hiring a lawyer for a guaranteed driver’s insurance was only after the police investigation period was over and after the actual arrest or prosecution process had taken place. However, the latest product covered attorney’s fees from the police investigation stage before prosecution. In addition, a product that allows relatively mildly injured patients with an injury grade of 14 to 8 to receive the cost of hiring a lawyer has been released.

After that, the market overheated as non-life insurers competed over the limit on the cost of hiring a solicitor. As concerns grew that the loss ratio could increase, as in real life medical insurance, an atmosphere was formed in the industry to be self-respecting.

The financial authorities saw that efforts to reduce guarantees at a time when market competition had already weakened would only add to the burden on consumers. In addition, there is an increasing possibility that the move to reduce insurance coverage, such as adding co-payments, will be used as marketing outside of the sale. In fact, as related reports came out, out-of-sale marketing was known to be underway. The marketing of the so-called ‘last train’ solicitation has started, saying that it is advantageous to buy driver insurance before July as there is a co-payment.

An official from the financial authorities said, “We confirmed that there is no plan to do so by checking whether policy changes that reduce drivers’ insurance have been implemented until recently.”

[저작권자 @머니투데이, 무단전재 및 재배포 금지]