If you’re looking for a quick solution to boost your credit ratings, you should be aware that no one strategy can miraculously enhance your numbers in a hurry. However, there are methods you may do that may help you improve your rankings in a pretty short period – it all depends on your unique scenario.

What Exactly Is a Credit Score?

A credit score is a numerical summary of your credit history that lenders use to determine the chance that you will repay any loans made to you.

The range of credit scores is 300 (poor) to 850 (outstanding). Higher credit scores reflect consistently positive credit records, such as on-time payments, modest credit utilization, and lengthy credit history. Lower ratings suggest that borrowers may pose a risk of investments due to late payments or excessive credit utilization.

There are no definite cutoffs for excellent or poor grades, but there are criteria for both. Most lenders consider scores over 720 to be optimal, while scores below 630 are considered hazardous.

Request a Credit Report

Examining your credit report is one of the most significant things you can do to enhance your credit score. Your credit score is a number that ranks your credit history, and your credit report is a comprehensive overview of your credit accounts and activities.

Examining your credit report can provide you with an overview of where your credit stands and what may be causing your credit score to fall. Having your credit history in hand or before your eyes, you will be able to see how many times you said to yourself “I need 500 dollars now with bad credit“, and you will also be aware of how much more you need to give back. With this information, you may devise a strategy to enhance your credit.

Each customer is entitled to a free credit report from each of the three credit agencies once a year under federal law. Since the epidemic began in 2020, all three credit agencies have provided free weekly credit reports.

Examine Your Credit Report For Mistakes

Once you obtain your credit reports, thoroughly review them. Your credit reports may be many pages large if you have a long credit history. It’s a lot to take in, particularly if this is your first time reading your credit report. Take your time, and if necessary, check your credit report over many days.

Keep Your Credit Utilization Ratio Below 30%

The credit usage ratio is calculated by comparing credit card balances to the total credit card limit. This ratio is used by lenders to assess how effectively you manage your money. A ratio of less than 30% and larger than 0% is typically seen as favorable.

Assume you have two credit cards with individual credit limits of $2,000 and $500 in overdue balances on one of them. The credit usage ratio for you would be 12.5%. In this scenario, add together your due debt ($500) and divide it by your overall credit limit ($4000).

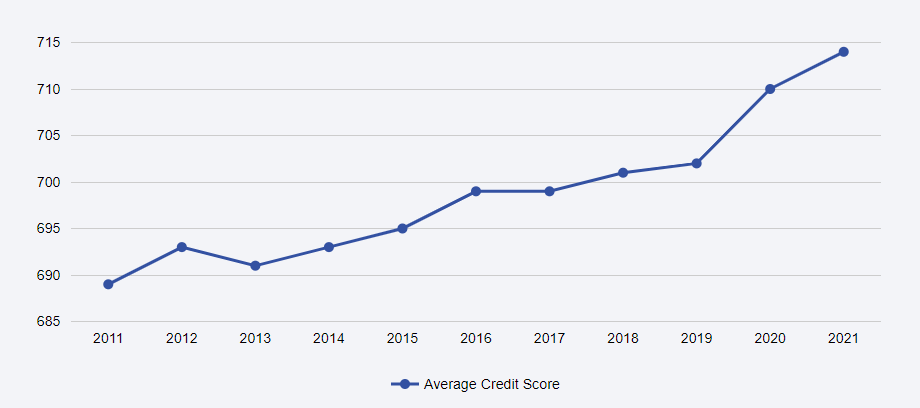

Although the year 2021 was still heavily affected by the pandemic the average FICO score in the US in 2021 was 714, a 4-point increase from the previous year. So we can assume that 714 is your goal, which you should strive for.

Set up Recurring Payments

As previously said, the most essential component in evaluating your credit score is your payment history. Addressing past-due payments on your credit record might help increase your score significantly. What’s more crucial is to be proactive to avoid missing payments in the future.

Make a Strategy For Paying All of Your Payments On Time

Payment history accounts for 35% of your credit score, therefore it’s critical to resolve late payments and establish future arrangements. Jacob claims it’s the first piece of advice she provides prospective customers.

You should also make paying off any credit card accounts in collections a top priority. You need to pay them off as soon as possible if you want to raise your score, since they’ll simply sit there until you do. Furthermore, you also should rearrange all your financial spending, and you need to be able to spend less money. It is very hard if you don’t have a professional who can help you with saving some amount. Nowadays, there are websites like mysavinghub.com where you can get information about sales and other staff that can make your wallet not be as empty as it could be.

If you need assistance developing a repayment strategy, Jacob suggests contacting a qualified financial planner or a credit counselor. You may find one via non-profit groups such as the Association for Financial Counseling and Planning Education and the National Foundation for Credit Counseling.

Make Yourself an Authorized User

Ask to be included as an authorized user if a member of your family or a friend has a credit card account with a high credit limit and a history of making payments on time. This adds the account to your credit reports, and its credit limit might assist you to maximize your use.

You may benefit from the primary user’s solid payment history if you have authorized user status, often known as “credit piggybacking.” The account holder is not required to grant you access to the card or even their account number for your credit to become better.

To obtain the best results, make sure the account reports to all three main credit agencies (Equifax, Experian, and TransUnion); most credit cards do.

Request a Credit Limit Increase

A bigger credit limit is another technique to lower your credit use ratio, which may help you improve your credit ratings. However, keep in mind that certain credit issuers do a severe credit check when you seek a credit limit increase, which might cause your credit to suffer.

Mix It Up

The different sorts of accounts in your credit reports are referred to as your credit mix. While it is unlikely to affect your credit score, lenders want to see a combination of revolving credit accounts (i.e., credit cards) and installment loans, such as mortgages, auto loans, and student loans. The more you diversify your borrowing, the better. Of course, taking out a loan you don’t need only to add some color to your credit mix is not a smart idea.

Conclusion

Repairing your credit might be a time-consuming process, but it is worthwhile in the end. You may accomplish this on your own or with the assistance of a credit repair firm.

Credit monitoring, on-time monthly payments, and good financial habits are essential to having excellent credit, regardless of which path you follow. The most essential thing is to remain patient and adhere to a tried-and-true technique.