Schufa Overhauls credit Scoring System with Transparency Focus

Table of Contents

GermanyS leading credit agency, Schufa, is set to introduce a revamped credit scoring system in the fourth quarter of 2025, emphasizing transparency and consumer understanding. The new model aims to replace the existing complex framework of industry and corporate scores.

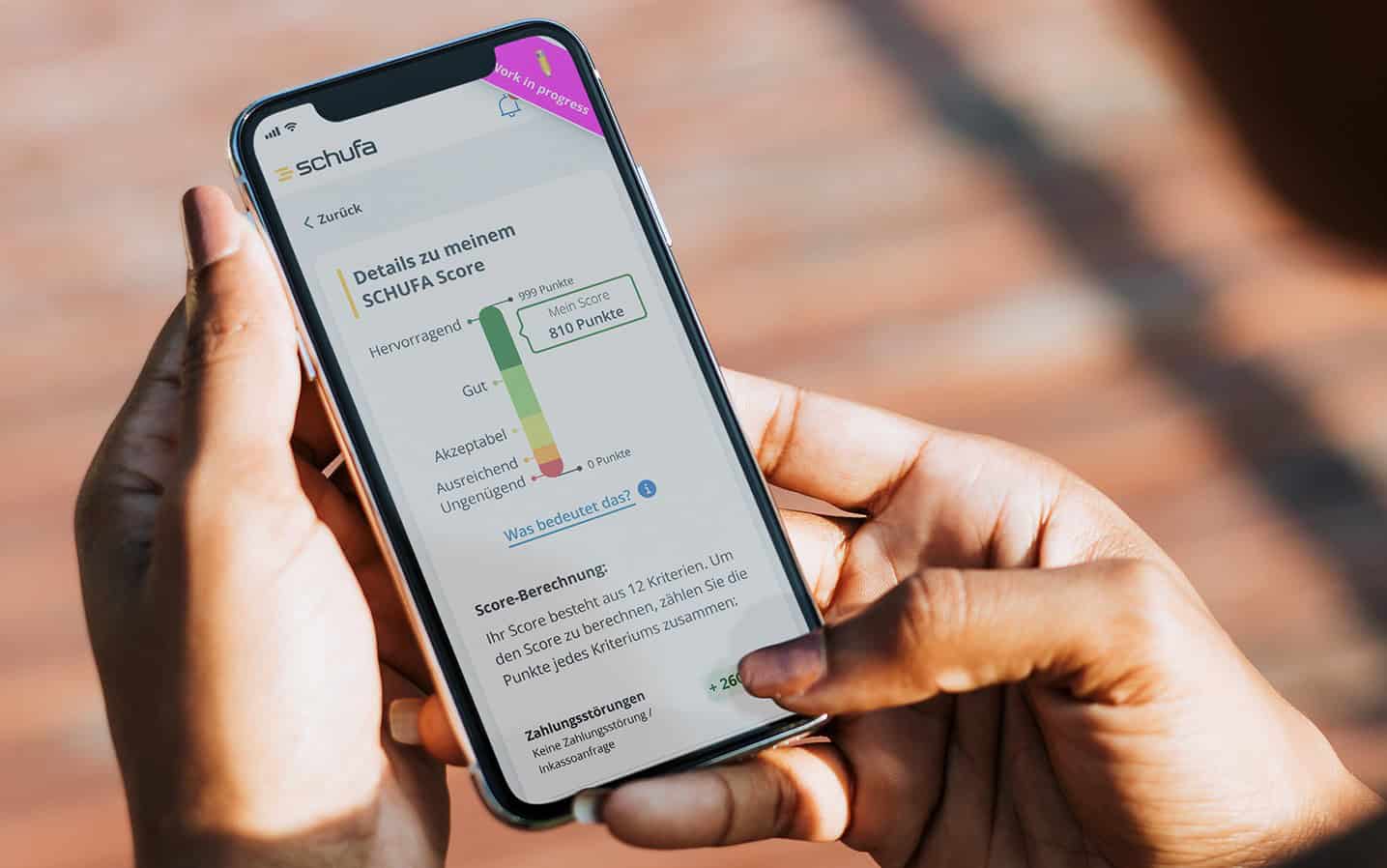

Currently, Schufa’s credit assessments rely on approximately 100 diverse criteria. The updated system will consolidate these into a simplified model based on just 12 key factors, utilizing a point system with a maximum score of 999. This change is designed to allow consumers to identify and understand the factors influencing their individual credit scores.

Schufa asserts that despite the simplification, the new scoring method will maintain a high level of predictive accuracy. The company reports that the Gini coefficient, a measure of the score’s effectiveness, will remain above 60 points, ensuring the model’s ability to accurately predict potential defaults.

Banks Testing New Credit Score Model

Seventeen banks are currently testing the new scoring system within their customer portfolios. Schufa plans to further optimize the model in the coming months before it fully replaces the current system. The rollout will be gradual,providing both businesses and consumers with simultaneous access to the new calculation method.

In conjunction with the new scoring system,Schufa intends to launch a digital account platform,providing consumers with free access to their stored data. An online tool will also be available, enabling users to calculate and interpret their credit scores.

While the basic credit score will remain free, the availability of a free daily score is still under consideration.

This reform is driven by both a desire for increased transparency and compliance with regulatory requirements. A recent European Court of Justice (ECJ) ruling in February 2025 mandated a clear and understandable presentation of scoring procedures.

Though, some critics argue that the specific weighting of the 12 criteria has not yet been disclosed, and the impact of factors such as loan usage requires further discussion.

Weighting of Criteria Still Under Wraps

Schufa reports that the weighting of individual criteria is currently undergoing testing. the specific point allocation for each factor and the handling of missing facts remain unclear. The 12 evaluation criteria include a history of defaults (unpaid invoices), the number and frequency of inquiries for checking accounts, credit cards, and telecommunications contracts. Loan terms, the age of the oldest credit card, and existing credit lines also factor into the evaluation.

Individuals with a long history of consistent payments will receive positive marks. This could pose a challenge for younger individuals or those new to the contry without an established credit history. Consumers with older banking contracts than those currently on file with Schufa may be able to improve their scores by providing updated information.

The new system will also consolidate inquiries for credit cards and checking accounts. Similarly, loan inquiries made within a 28-day period will be bundled, preventing consumers from negatively impacting their scores when shopping for the best rates on loans, such as mortgages. Factors such as real estate loans,guarantees,and the age of the current address will also be considered,but the number of previous moves or the living environment will not.

it remains to be seen whether successfully repaying a loan will have a more positive impact on the score than having no debt at all.

Increased Transparency: A Fairer System?

Schufa aims to provide consumers with greater traceability and control through the new scoring system. The simplified calculation method and the ability to self-assess are intended to promote fairness in credit assessments. However, the practical acceptance of the new score by businesses and consumers remains to be seen. Some individuals may experience negative impacts or inaccurate assessments due to incomplete data. Schufa plans to streamline the process of supplying or correcting incomplete information.

“The new Schufa score is the best qualitatively and most understandable score that we were able to develop on the basis of our market-leading database. The requirement was: to achieve the best possible forecast bag under the side condition of the traceability for consumers.”

the inclusion of modern payment methods like Buy Now, Pay later (BNPL) and the consolidation of loan inquiries within a 28-day window are positive developments. The elimination of discrepancies in information provided to businesses and consumers is also a step forward, possibly simplifying loan negotiations. The provision of explanatory tools will further enhance traceability, demonstrating how individual criteria impact the score based on personal data.

absolutely! Here’s the Q&A-style blog post based on the provided article, designed for high quality, engagement, and SEO:

Schufa’s Credit Score Overhaul: Your questions Answered

(Introduction)

Q: What is Schufa and why is this credit score update significant?

A: Schufa, or “Schutzgemeinschaft für allgemeine Kreditsicherung” (Protection Association for General Credit Security), is Germany’s leading credit rating agency. It’s the gatekeeper of creditworthiness details for a vast majority of German citizens. This means Schufa’s scores significantly influence whether you get a loan, a credit card, a phone contract, or even a rental agreement. The update coming in Q4 2025 is a major overhaul meant to increase openness and align with new European regulations.

(Core Changes & Benefits)

Q: What are the key changes coming to Schufa’s scoring system?

A: The current system, which uses approximately 100 different criteria, is being streamlined into a model based on just 12 key factors. These factors will be used to calculate a score on a scale of 0-999. The primary goals are to make the system more understandable for consumers and to comply with recent rulings by the European Court of Justice (ECJ) mandating clearer credit scoring procedures.

Q: How will this new system benefit consumers?

A: The main advantages center on increased transparency and control. By focusing on 12 key factors, consumers can more easily understand how their financial behavior impacts their score. Schufa plans to launch a digital platform and online tool that will allow users to access and interpret their scores. This shift will empower individuals to take informed steps to improve their creditworthiness.

Q: Will the new scoring system be less accurate?

A: No. Schufa asserts that the new scoring method will maintain a high level of predictive accuracy. They cite that the Gini coefficient, a measure of how well the score predicts loan defaults, will remain above 60 points.

(Technical Details and Implementation)

Q: How will the new Schufa score be calculated? What Factors are included?

A: The exact weighting of the 12 factors is still in testing. It is indeed known that the factors will include:

History of defaults (unpaid invoices).

the number and frequency of inquiries for checking accounts, credit cards, and telecommunications contracts.

Loan terms.

the age of the oldest credit card.

Existing credit lines.

Real estate loans.

guarantees.

The age of the current address.

It’s important to note: the number of previous moves and your living environment will not be considered.

Q: When will this new schufa system be fully implemented?

A: The new scoring system is scheduled to launch in the fourth quarter of 2025, with a gradual rollout. 17 banks are currently testing the new scoring system. the migration will be gradual to minimize disruption and allow both businesses and consumers to adapt. Schufa plans to make the new calculation method available concurrently to both groups.

Q: Will the new system include modern payment methods?

A: Yes. The new system will consider modern payment methods like “Buy Now, Pay Later” (BNPL) offerings. Loan inquiries made within a 28-day period will be bundled to avoid penalizing consumers who shop for the best rates.

(Potential Challenges and Considerations)

Q: are there any potential drawbacks to the new system?

A: While the goal is greater transparency, it remains to be seen if the new system is fairer for all individuals. Some individuals may experience negative impacts or inaccurate assessments due to incomplete data. For consumers with older banking contracts that are not in the Schufa system, it’s possible to improve your score with more information. Schufa is expected to streamline the process of supplying or correcting incomplete information.

Q: Can I check my Schufa score for free?

A: The basic score will remain free of charge. Whether a free daily score will be offered is still under consideration.

(expert Insights & Also to be considered:)

Q: What is the overall importance of this reform?

A: Credit scoring is a fundamental for many aspects of life in Germany, and this overhaull represents a move towards consumer empowerment.The drive for greater transparency and control by bringing transparency to the scoring process by simplifying it, makes it easier for consumers to understand the factors that influence their creditworthiness.

Q: What are some of the potential changes to credit reporting?

A: The update emphasizes transparency. The elimination of discrepancies in information provided to businesses and consumers is designed to simplify loan negotiations. The provision of tools to explain credit scores will enhance traceability.

Final Thoughts

The new Schufa system promises a more equitable and informative way to navigate credit assessments. By understanding the key factors and taking proactive steps to manage your finances, you can potentially improve your creditworthiness and access a wider range of financial products and services.