Pakistan Stock Exchange Plunges to Record Low Amid Geopolitical Concerns

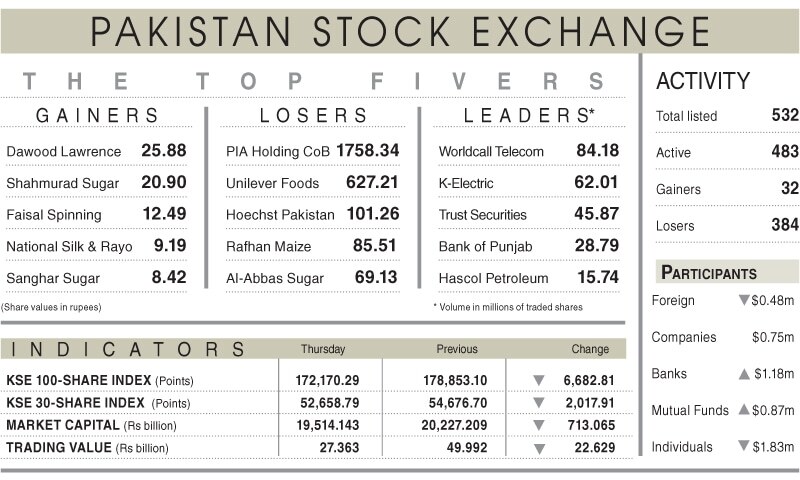

Karachi – The Pakistan Stock Exchange (PSX) experienced its most significant single-day decline in history on Thursday, , as mounting geopolitical tensions and rising global oil prices triggered a widespread sell-off. The benchmark KSE-100 index closed at 172,170.29, down 6,683 points, or 3.74%, wiping out approximately Rs713 billion in market capitalization during the first session of Ramazan.

The dramatic fall was spurred by concerns over escalating tensions between the United States and Iran, leading to a spike in international crude prices – up over 6% in two days. As a net oil importer, Pakistan is particularly vulnerable to higher energy costs, exacerbating existing macroeconomic anxieties and eroding investor confidence. The index touched an intraday low reflecting a drop of 7,205 points, demonstrating the intensity of the selling pressure and volatility.

Regional Instability and Domestic Political Factors

Analysts point to a confluence of factors contributing to the market’s downturn. Farid Alam of AKD Securities noted that investors reacted swiftly to perceived regional instability, referencing reports of a potential US attack. Pakistan’s geographic proximity to conflict zones and its inherent economic vulnerabilities amplified market anxiety. Heightened domestic political tensions, including reported sit-ins and roadblocks, further dampened investor sentiment.

While data from the Securities and Exchange Commission of Pakistan indicated the exit of 125 foreign companies, Alam cautioned against interpreting this as a sudden capital flight. He explained that a detailed breakdown revealed many of these firms were dormant, project-based, or undergoing restructuring. He emphasized that headlines can disproportionately affect sentiment, even when underlying fundamentals remain relatively stable.

Market Manipulation and Investor Advice

Addressing concerns about potential market manipulation, Alam stated that declines of this magnitude are typically driven by broader sentiment shifts, leverage unwinding, and macroeconomic risks rather than coordinated actions by large players. He advised small and new investors to avoid panic selling during periods of extreme volatility.

Corporate Results and Foreign Outflows

Mohammed Sohail, Chief Executive of Topline Securities, attributed the downturn to reports of delays in the Reko Diq project, aggressive foreign selling, and corporate results that fell short of expectations. Persistent foreign corporate outflows added to the downward pressure, with local insurance companies also emerging as significant sellers.

Trading Volume and Sector Impact

Shortened trading hours due to Ramazan contributed to reduced participation and amplified price swings. Trading volume decreased by 22.17% to 543 million shares, while traded value plunged 45.26% to Rs27.39 billion. Index-heavy stocks, including Fauji Fertiliser Company, Engro Holdings, United Bank Ltd, Oil and Gas Development Company, Pakistan Petroleum Ltd, and Meezan Bank, collectively erased 2,113 points from the benchmark.

Corporate Earnings and Market Outlook

Faysal Bank reported CY25 earnings of Rs22.5 billion (earnings per share of Rs14.80), a 6% year-on-year decrease. Quarterly profit stood at Rs6.5 billion, up 83% year-on-year and 17% quarter-on-quarter. The bank announced a cash dividend of Rs2 per share, bringing its total CY25 payout to Rs6.5 per share.

Technical Analysis and Future Resistance

Financial and technical analyst Khalid Saifuddin suggested the market had already factored in most positive catalysts and reached historic highs, making it susceptible to correction. He described the earlier rally as a “bull trap” and Thursday’s decline as a release of accumulated pressure. Saifuddin highlighted political uncertainty, cross-border tensions, and heightened regional risk perceptions, particularly related to US-Iran developments, as amplifying volatility.

Investors are also closely monitoring the outcome of the prime minister’s engagement with US leadership, as ambiguity regarding Pakistan’s geopolitical positioning tends to unsettle markets. Upcoming external payment obligations, including a maturing Eurobond in April, are also contributing to market volatility.

Analysts anticipate the 172,000-170,000 range will serve as critical support levels, while 180,000 has emerged as immediate resistance for any potential recovery attempt. The market’s fragility underscores the sensitivity to both domestic and international developments, requiring careful monitoring in the coming weeks.