To mitigate the requirement to change from a multiple technology evaluation to a single evaluation, the financial authorities plan to announce an improved special listing system next month. The plan aims to reduce the time and cost of listing for companies in industries that fall under state-led strategic technology. The system improvement plan will include easing the requirement for technology evaluation from multiple evaluations to a single evaluation. This will benefit industries such as AI semiconductors, secondary batteries, displays, advanced mobility, and robots. The improved system will allow companies in these industries to raise funds more efficiently. The plan also includes measures to strengthen the sharing of information between the exchange and the Financial Supervisory Service. However, it is important to note that this does not mean that the threshold for listing will be eased or that all companies will be eligible for listing. The purpose of the plan is to streamline the listing process for companies in select industries. The introduction of a special technology listing system dedicated to deep technology companies has been suggested by the Venture Capital Association. However, the exchange believes that it is more efficient to make selective improvements to the existing system rather than creating a separate listing system for specific industries. The stock prices of companies listed on special technology exemptions have been a concern. While there has been an increase in IPOs, investor confidence in these companies appears to be declining. Only 62 out of 183 companies listed on the special list saw their stock prices rise from the day of listing, and less than 30% achieved double-digit gains. Examples of inflating future earnings forecasts have contributed to this lack of confidence. To address these issues, the financial authorities plan to include measures to strengthen public disclosure in the improved system. This includes disclosing the technology development status and performance of companies subject to special technology exemptions. The responsibility of listing supervisors will also be strengthened, and penalties for organizers who engage in misleading actions will be discussed. The aim is to protect investors and restore trust in the special listing system.

Includes a plan to mitigate the requirement to change from a multiple technology evaluation to a single evaluation

Of the 183 companies listed on special technology cases, only 62 companies saw their stock prices rise from the day of listing

Examples of inflating future earnings forecasts… Disclosure and preparation of measures to strengthen supervisors’ responsibility

In order to revive the enterprise industry which has entered the ice age, the financial authorities are starting to breathe new funding. The key is to find companies directly and actively publicize the ‘special technology listing’ system. This is because companies are deemed not to be using a system that can raise money even without sales or profit properly. Furthermore, the financial authorities intend to support the smooth listing by announcing a plan to improve the special listing system next month.

Individual technology evaluation for companies such as AI semiconductors and secondary batteries… System improvement plan announced in July

According to the financial investment industry, the financial authorities intend to include a plan to ease the requirement to change from multiple evaluation to a single evaluation for technology evaluation in industries that fall under state-led strategic technology in a plan to improve the special listing system to be published next month. The purpose is to help companies struggling to raise money by reducing the time and cost of listing. For industries subject to individual evaluation, the financial authorities, the Ministry of Trade, Industry and Energy, and the Ministry of Science and ICT have made detailed adjustments. It is expected to include industries such as artificial intelligence (AI) semiconductors, displays, advanced mobility, secondary batteries, and robots.

A special technology listing refers to a promising technology company with outstanding technology that qualifies for listing by receiving a technology evaluation from a professional evaluation agency. Even if there are no sales or profits, as long as the technology is proven, it can enter the KOSDAQ market. Technology evaluations must be received from multiple professional evaluation agencies, and minimum A and BBB reviews are required for listing. However, the Korea Exchange made exceptions for the materials, parts and equipment industries (deposit manager). If you receive a result that meets the minimum grade (grade A) from one assessment organisation, you can go on the list.

see the original icon

With this improvement in the system, it is expected that companies belonging to the industries designated by the government will be able to raise funds by saving the time and cost of listing. This is because the process, which was burdensome from the companies’ point of view, will disappear as this improvement plan also includes a plan to strengthen the sharing of information between the exchange and the Financial Supervisory Service.

However, it is explained that it does not pave the way for listing for some companies or ease the threshold for listing. Meanwhile, the Venture Capital Association has argued that a special technology listing system dedicated to deep technology (innovative technology-based companies) needs to be introduced. As the special technology listing was initially introduced to foster the bio industry, the rationale was that an independent listing route was needed to foster the deep technology industry. Regarding this, an official from the exchange said, “In order for companies to be listed quickly, we should take it as a concept to overhaul unreasonable parts that they don’t have to go through in the listing process.” Because it is made so that it can be applied selectively, there is no need to prepare a listing system for a specific industry.” He added, “It is a misunderstanding to continue to see the technology exemption system as a listing system for bio-companies only.”

The company was out of breath, but … ‘Sigh’ just by looking at the stock price

It is true that the special technology listing system has been introduced to help in the smooth listing of bio companies. In the case of bio companies developing new drugs, it takes longer than companies in other fields to confirm their technology as sales, but this is because they need a lot of money for clinical trials and research and development.

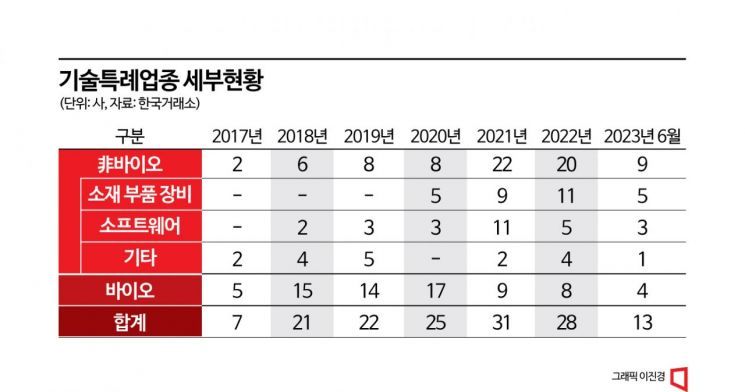

However, since 2014, it has opened the door for special technology listings to non-bio companies, and has now established itself as a funding channel for companies with technological capability and growth potential. Starting with Ast, an aircraft parts manufacturing company in 2014, 79 non-bio companies have established themselves in the KOSDAQ market by using the special technology listing system. From 2021, there have been more applications for special technology listing from non-bio companies. In 2021, 9 bio companies were listed, but 22 non-bio companies entered the market. In 2022, there were 8 bio companies and 20 non-bio companies. In the first half of this year, there were 4 bio companies and 9 non-bio companies.

see the original icon

However, the problem is the stock price of these companies. IPOs are on the rise, but investor confidence in companies listed on special technology exemptions appears to be declining. After passing the technology evaluation, companies self-estimate future performance to determine the public offering price. However, there are many cases where the estimated future corporate value at the time of listing has not actually been shown. Of the 183 companies listed on a special list through KOSDAQ technology, 62 companies maintained a positive stock price compared to the listing date, less than half of them. Only 55 companies (around 30%) achieved double digit gains.

For example, Enzychem Life Sciences, a new drug development company listed and transferred from the KONEX market to the KOSDAQ market in February 2018 through a special technology listing, has never made a profit since its listing. It recorded an operating loss of 14.3 billion won in 2018, but even after that, 2019 (-16.4 billion), 2020 (-19.1 billion), 2021 (-20.7 billion won), and 2022 (-14.6 billion) won to all sluggish. In the first quarter of this year, it records an operating loss of 3 billion won. Not only this. An expected result is that it is difficult to expect an immediate operating profit, but very late public announcements such as stopping clinical trials, stopping the increase of capital paid by main shareholders, and the late production of the Corona 19 vaccine are also adverse. affect stock price. Based on the revised stock price, the closing price on the listing day was 13,131 won, but as of the 21st, the closing price was 1,585 won, down about 88%.

There are a number of companies that have already been designated as control stocks. Controlled stocks refer to the designation of candidates at risk of delisting by the exchange and notification of investors. Financial authorities apply more lenient standards than general KOSDAQ listed companies for continued listing taking into account the characteristics of technology-listed companies in particular.

Listed companies subject to special technology control are controlled if any of the following reasons occur: ‘Sales less than 3 billion won’ designated as an item. If the same situation continues after that, it will lead to delisting. Currently, among the listed companies subject to special treatment, Intromedic, Innosis, and Earth & Aerospace have been designated as control stocks. There are a total of 4 places including Cellivery.

In Intromedic’s case, the Exchange’s Corporate Review Committee is currently reviewing whether to delist. In January this year, Uneco (formerly Eco Meister, listed in 2018), a waste treatment company, was delisted for the first time as a company listed on special cases for technology. At the time of listing, Uneko presented a corporate value of more than 100 billion won with the hope of reaping a net profit of 8.4 billion won in 2018, 11.3 billion won in 2019, and 16 billion won in 2020. However, in reality, it appeared to be -37.5 billion won in 2019, -19.4 billion won in 2020, and -4.2 billion won in 2021.

Strengthen disclosure of technology development status, discuss penalties for organizers, etc.

The financial authorities intend to protect investors and restore trust by reducing the side effects of the special listing system by including content such as strengthening public disclosure in the system improvement plan. The key is to strengthen the performance disclosure or technology development status of companies subject to special technology exemptions and strengthen the responsibility of listing supervisors (securities companies). When calculating the public offering price, it is confirmed that the stock manager prepares measures to strengthen the real responsibility of the listing manager, such as preventing actions such as excessively inflating the ransom by cooperating with securities companies and managing the stock price for success. of the IPO done.

An official from the financial investment industry said, “Constantly disclosing technology after listing can serve the purpose of providing information to investors, but it also has negative effects, such as disclosing a company’s technology to competitors.” “Exchanges and financial authorities are also taking measures to protect investors. I will think about the middle point with

Reporter Lee Min-ji ming@asiae.co.kr

If the top news you have to see is dropped, ‘National Family Breakdown Day’… 4.6 million sex buyers… mask man

#months #announcement #improvement #plan #special #technology #listings #Subsequent #management #investor #protection #remain #challenges